Cross-border E-commerce

As an import and export service provider for customers in cross - border e - commerce, Zhongshen International Trade mainly assists cross - border e - commerce enterprises in handling the import and export processes of goods.

As an import and export service provider for customers in cross - border e - commerce, Zhongshen International Trade mainly assists cross - border e - commerce enterprises in handling the import and export processes of goods.

Chinas cross - border e - commerce has witnessed rapid growth, making China one of the countries with a complete global e - commerce ecosystem. Platforms such as Shein and Temu have shaken the global shopping market, and the influence of Chinese e - commerce has been felt in places like South Korea and the United States. It is expected that the global e - commerce sales will continue to grow, and China is expected to maintain its leading position. Chinas efficient and innovative logistics has promoted the acceleration of cross - border e - commerce, enabling Chinese - made products to reach the world.

Brazils Tax Compliance Program (PRC) is an important adjustment to the e - commerce market, bringing new challenges and opportunities to cross - border sellers. Against this background, sellers need to adapt to the new tax environment, optimize business strategies, and at the same time, take advantage of the policies to better explore and utilize the growth potential of the Latin American market.

This article deeply analyzes the process, advantages and disadvantages, as well as the key precautions for the implementation of the 9610 cross - border e - commerce import model. It comprehensively analyzes the application and practice of this model in the cross - border e - commerce field from different dimensions, providing valuable reference and inspiration for practitioners.

This article elaborately analyzes the tax policies for cross - border e - commerce retail imports, including the scope of application, current policies, tax calculation methods, and restrictive conditions. The article also compares the tax differences between cross - border e - commerce retail imports and general trade methods through an example of purchasing French red wine.

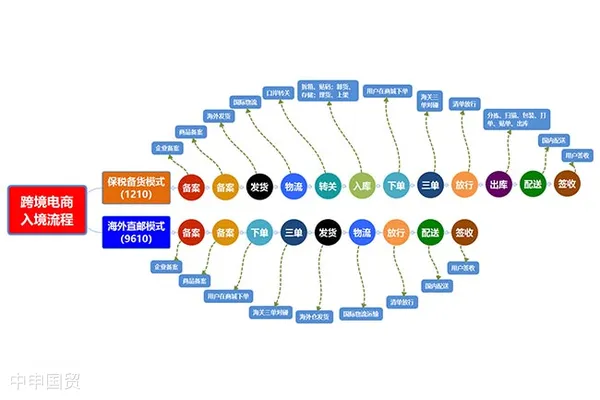

The cross - border e - commerce import customs clearance mode is undergoing a transformation. From purchasing on behalf of others to overseas online shopping, and then to the bonded mode, each mode has its characteristics and target audiences. Now, with the adjustment of national policies, which of these modes will continue to exist and which will gradually be marginalized? Lets take a look at the secrets of these four modes. Perhaps you will find that the future of cross - border e - commerce is not far away.

With the rise of e - commerce, cross - border e - commerce business has become an important part of international trade. This article provides a detailed analysis of three customs clearance modes for cross - border e - commerce business: direct purchase import (9610), retail export (9610), and business - to - business export (9710, 9810), and also introduces which products can be imported through cross - border e - commerce channels.

In 2022, the import and export volume of Chinas cross - border e - commerce exceeded 2 trillion yuan, a year - on - year increase of 7.1%. Cross - border e - commerce has become an important part of Chinas foreign trade, but the accompanying compliance risks cannot be ignored. The prosperity of the industry requires policy support and a standardized regulatory system. At the same time, enterprises also need to improve their compliance awareness to ensure sustainable and healthy development.

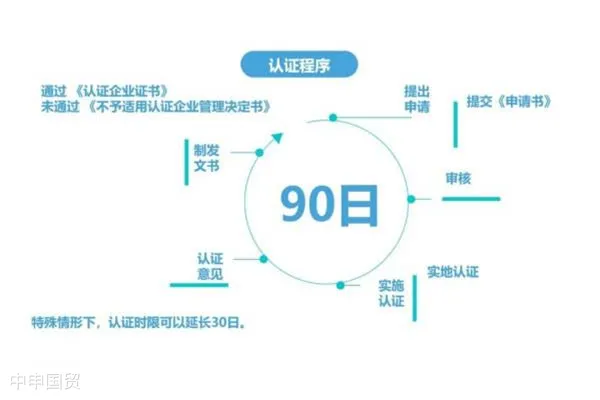

With the increasing development of cross - border e - commerce trade, more and more cross - border e - commerce enterprises are seeking to go global. Against this background, the policy support and international mutual recognition advantages of the AEO system will provide boosters and passes for cross - border e - commerce enterprises. Various cross - border e - commerce enterprises need to choose the applicable AEO certification standards for self - assessment according to their own types and responsibilities, and get ready to go global smoothly.

In the process of operation, cross - border e - commerce faces complex tax issues. On the basis that an enterprise can provide valid input vouchers (invoices), the tax authority can quickly determine the enterprises income (net profit), and then the enterprise can pay corporate income tax according to the net profit and the income tax rate. However, many cross - border e - commerce enterprises do not have input invoices in actual operation.

? 2025. All Rights Reserved. 滬ICP備2023007705號-2  PSB Record: Shanghai No.31011502009912

PSB Record: Shanghai No.31011502009912