With the approach of the carbon tariff transition period, Chinese export enterprises are facing a series of challenges and response needs. This article will provide a detailed interpretation of the implementation rules and calculation logic of the EU carbon tariff transition period to help export enterprises better prepare and respond.

I. Key Points of the Carbon Tariff Transition Period

1) Core Content of the Implementation Rules during the Transition Period:The European Commission recently announced the implementation rules for the carbon tariff transition period, providing some reference for non - European export enterprises. These rules mainly include monitoring, calculating and reporting on the direct/indirect emissions of facilities, the direct/indirect attributable emissions in the production process of CBAM products, the usage and embedded emissions of CBAM product precursor materials, etc.

2) Explanation of Key Terms:Before preparing to respond to carbon tariffs, export enterprises need to clearly understand several key terms, such as facilities, precursor materials, production process, attributable emissions and embedded emissions. These terms define the basic framework for carbon tariff calculation.

3) Calculation Logic:After understanding the key terms, export enterprises need to master the overall logic of carbon tariff calculation. This includes how to calculate from facility emissions to attributable emissions in the production process, and then to embedded emissions of CBAM products.

II. How to Monitor, Calculate and Report Carbon Tariff - Related Matters

1) Emission Monitoring of Facilities:First of all, export enterprises need to monitor the emissions of their facilities. This includes all direct and indirect carbon emissions generated during the production process of the facilities. Direct emissions mainly come from production activities, while indirect emissions may come from power consumption, transportation, etc.

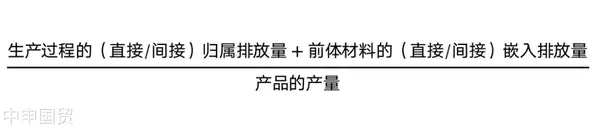

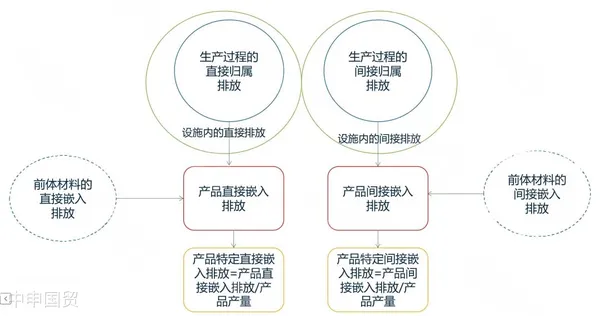

2) Calculation of Attributable Emissions and Embedded Emissions:Secondly, based on the facility emission data, enterprises need to calculate the attributable emissions in the production process and the embedded emissions of CBAM products. This requires clarifying the usage of each precursor material in the production process, as well as the direct and indirect embedded emissions brought by these materials.

3) Data Reporting and Audit:Finally, enterprises need to report all the collected and calculated data. This may require third - party audit to ensure the accuracy of the data. At the same time, the data will also be used to calculate the carbon tariffs that enterprises need to pay.

III. Response Strategies for Export Enterprises

1) Advance Preparation and Assessment:Facing the approaching of the carbon tariff transition period, export enterprises need to prepare as early as possible. This includes assessing their own carbon emission status and the additional costs that may be incurred due to carbon tariffs.

2) Optimize the production process:After understanding their carbon emission status, enterprises can reduce carbon emissions by optimizing the production process. This can not only reduce the cost of carbon tariffs but also potentially enhance the market competitiveness of the enterprise.

3) Maintain communication with EU authorities:In addition to internal preparations, export enterprises also need to maintain close communication with relevant EU authorities. This helps enterprises to more accurately understand the latest developments of carbon tariffs and the specific regulations that may affect them.

Through the preparations and responses in the above three aspects, export enterprises will be more likely to successfully meet the various challenges brought about by the carbon tariff transition period.

Tags: CBAM Foreign Trade Documents Trade Essentials

? 2025. All Rights Reserved. 滬ICP備2023007705號-2  PSB Record: Shanghai No.31011502009912

PSB Record: Shanghai No.31011502009912